![Beyond The Microfinance Challenges II… Is The Financial Sector In Crises? [Article]](https://nsemgh.com/wp-content/uploads/BoG-Building.jpg)

The least any business owner will do is to deliberately undertake transactions to undermine the future of his or her company that he or she has labored to build. The most basic financial impulse in to invest for the future, because the future is so unpredictable. But the bare fact is, not many of us get through life without having a little bad luck. Sometimes huge losses: Like results of the financial crises from 2013 to date. Risk teaches us that there are always unforeseeable events in the future, which will never lose their capacity to take us by surprise. Like the great depression in the 1930s 40s and the 2008 financial meltdown in the US.

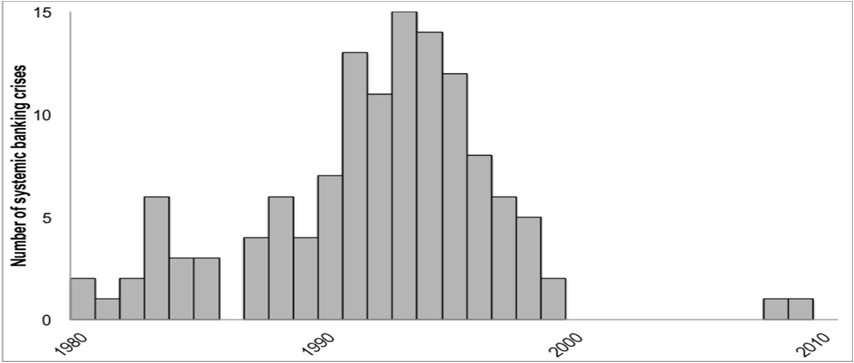

A recent review by the International Monetary Fund (IMF) revealed that over 133 member countries had experienced significant banking sector problems from the 1980s and Africa had its fair share. Banking crises are not a new economic phenomenon, and similarly are not the only source of financial crises. Over the course of the past two centuries there have been a surprisingly large number of financial crises, as demonstrated in the attached figure. In understanding banking crises over time, it is useful to identify the causes in context with historic examples of banking collapses.

Figure 1. Banking crises in Africa From 1980 – 2010

Source: Laeven and Valencia, 2008

In June 2016,I gave a contrarian, comprehensive account of the banking crisis, both its origin and extent but I also explained how the deeper problem was a type of public policy-making failure.

I’ve offered my own assessments, and obviously, I consider them valid. Decide for yourself.

“The failure in the microfinance sector is just a microcosm of greater challenges facing the overall financial sector. It is also believed that a number Non-Bank Financial Institutions (NBFI) are facing similar challenges and it is only time will tell when the authorities will have another set of challenges on their hands. Banks are quickly approaching their “automation tipping point,” and they are downsizing in the past three years, some on the quiet and others are in public domain. A case point is Standard Bank Ghana.”

The above is a quote from an article published in B&FT newspaper in June 2016. Fast forward 2019, so far, the central bank has revoked the license of 420 financial institutions on the grounds of insolvency.

- 347 microfinance institutions license has been revoked.

- Licenses of 9 insolvent banks were revoked. Others were merged to reduce the number from 33 to 23.

- 15 savings and loans companies, eight (8) finance house companies, and two (2) non-bank financial institutions that had already ceased operations.

- Security and Exchange Commission (SEC) has revoked the license of 5 Investment Banks and voluntary cessation of operation by 6.

- SEC is investigating 21 Fund Managers whose depositors’ funds of about 5 billion cedis are tied up.

Banking crises can be caused by inadequate regulatory oversight, government policy failure, macroeconomic instability, bank runs, positive feedback loops in the market and contagion.

Conditions Leading up to the Banking Sector Crisis from 2012 – 2016

Growth Trends After 2012

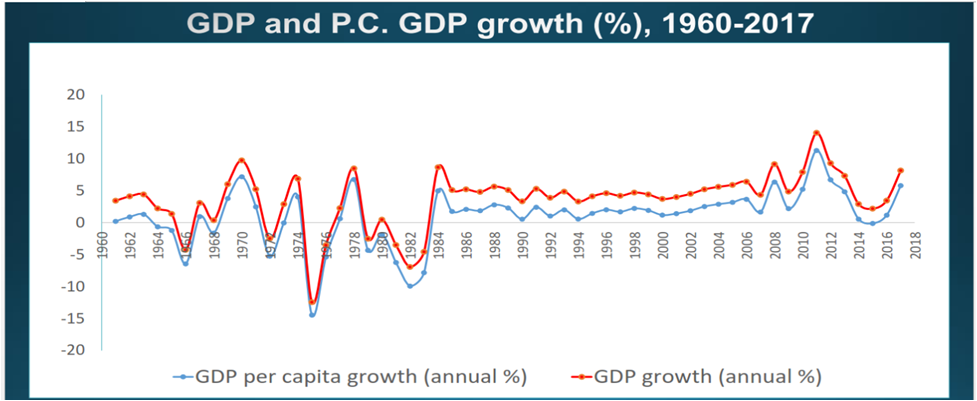

On a macroeconomic level, generally, Ghana had a steady growth up 2012 when growth started slowing to the lowest since the fourth republic.One major indicator of a country’s macroeconomic performance is real GDP growth. Ghana’s growth record was quite erratic prior to the mid-1980s when the country embarked on economic reforms.

From a reasonably high GDP growth of 11% in 2011, the economy of Ghana began to record a consistent year on year slowdown in GDP growth reaching the lowest of 3% in 2016. The performance of the financial sector of our country depends on the performance of the larger economy and the sluggish growth of the economy has made many businesses unprofitable rendering borrowers unable to repay their loans. Lower rate of non-performing loans indicates the improvement in the real economy of the country and the opposite is also true.(see Figure 2).

Source: World Bank data

2012 Election Year Economic Shock

For the past 30 years Ghana records an average 6.5% budget deficit but in 2012 Ghana recorded 12% budget deficit, which is the highest ever recorded in the fourth republic. Despite the huge budget deficit, shortfall in Government’s revenue performance, culminated in Government’s decision to go the IMF in 2014 for balance of payment support. Coupled with 4 years of ‘DUMSOR’, the country never really recovered from 2012 economic shocks.

source: